Wood Plastic Composite (WPC) Market Benefits from Plastic Waste Recycling Trends 2032

Global Wood-Plastic Composite (WPC) Market Set for Robust Growth: Poised to Surge from USD 8.06 Billion in 2024 to USD 20.25 Billion by 2032

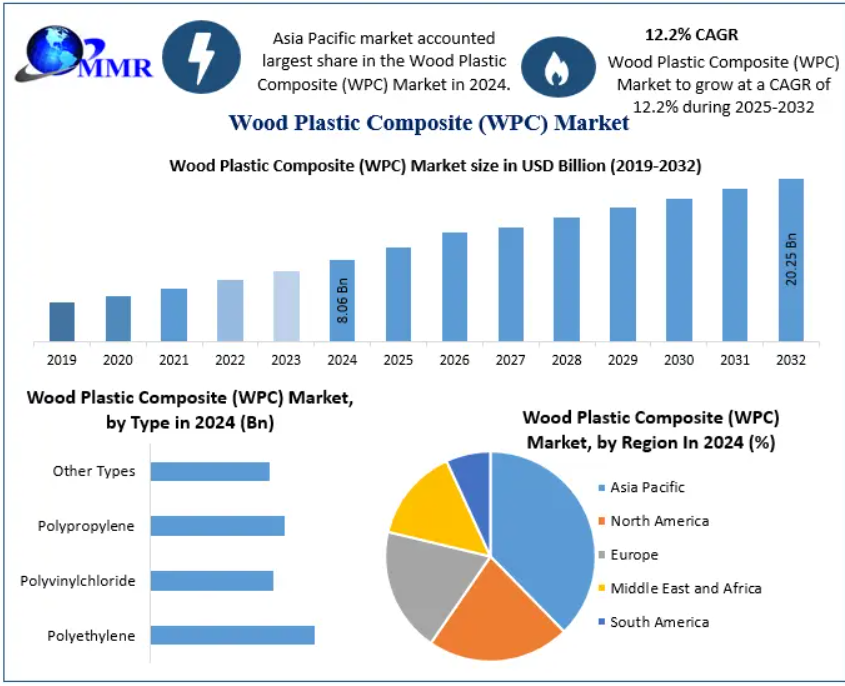

Market Estimation & Definition

The Global Wood-Plastic Composite (WPC) Market—an industry that blends natural wood fibers with synthetic polymers to produce highly durable, sustainable, and versatile materials—is gaining significant momentum. In 2024, the market is valued at USD 8.06 billion and is expected to grow at a compound annual growth rate (CAGR) of 12.2%, reaching nearly USD 20.25 billion by 2032.

Wood-plastic composites are engineered materials made by combining wood flour, wood fibers, or sawdust with thermoplastics such as polyethylene, polypropylene, or polyvinyl chloride. The result is a material that combines the natural look and feel of wood with the resistance and durability of plastics. Their strength, low maintenance requirements, and eco-friendly properties make them highly appealing in construction, automotive, and consumer applications.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/76219/

Market Growth Drivers & Opportunities

Sustainability and Environmental Awareness

Growing global demand for sustainable and environmentally conscious materials is one of the strongest drivers of the WPC market. These composites incorporate recycled plastics and wood waste, reducing pressure on deforestation while promoting circular economy principles. Governments and consumers alike are increasingly supporting eco-friendly construction and product design.

Resilience and Low Maintenance

Unlike traditional wood, WPCs are resistant to rot, decay, termites, and moisture damage. They require far less maintenance than conventional wood, making them especially suitable for outdoor applications such as decking, cladding, and fencing. This durability and cost-effectiveness over the product lifecycle strengthen their market appeal.

Expansion of Construction and Renovation Activities

The construction industry is a primary consumer of WPC products. With the surge in home renovation projects, growing urbanization, and rising infrastructure development, WPC adoption has soared. The demand for decking and outdoor applications in residential and commercial spaces is particularly notable.

Innovation and Technology Advancement

Technological progress has allowed manufacturers to experiment with advanced blends and surface finishes. New techniques have improved the aesthetics, strength, and customization options of WPCs. Beyond construction, the automotive sector is leveraging WPCs in interior parts and lightweight components to meet efficiency and sustainability goals.

Emerging Opportunities

- Green Building Initiatives: Stricter environmental standards and certifications provide a favorable regulatory environment for WPC adoption.

- Automotive Industry Growth: As manufacturers seek lightweight, durable alternatives, WPCs are being integrated into dashboards, trims, and panels.

- Infrastructure Development: WPC’s use in public infrastructure, such as benches, walkways, and outdoor furniture, presents fresh opportunities.

- Recycling and Circular Economy: Increasing emphasis on recycling plastic waste is expected to boost WPC production further, strengthening its sustainable market positioning.

Segmentation Analysis

The market is segmented into type, application, and end-use industry, each reflecting diverse adoption trends.

By Type:

- Polyethylene-Based WPCs: The largest share of the market comes from polyethylene composites, valued for flexibility, recyclability, and cost efficiency. They dominate decking and railing applications.

- Polyvinyl Chloride (PVC) WPCs: Offering rigidity and excellent resistance to water, PVC-based composites are ideal for applications like window frames, fencing, and marine decking.

- Polypropylene WPCs: Known for their high strength-to-weight ratio, polypropylene-based composites find use in more specialized applications, including automotive interiors and industrial parts.

- Others: This segment includes composites based on specialty polymers, designed for niche markets where higher performance, durability, or heat resistance is required.

By Application:

- Building & Construction Products: This is the largest application segment, with WPCs used extensively in decking, fencing, cladding, roofing, and interior construction. Their low maintenance and aesthetic appeal make them a preferred choice for modern construction.

- Automotive Components: The automotive industry increasingly uses WPCs for dashboards, trims, door panels, and load-bearing components, leveraging their lightweight and eco-friendly properties.

- Industrial & Consumer Goods: WPCs are also used in furniture, household products, packaging, and industrial tools, offering durability and environmental benefits.

- Others: Additional uses include marine applications and specialty manufacturing where moisture and weather resistance are crucial.

By End-Use Industry:

- Residential: Residential construction and renovation, particularly outdoor decking, fencing, and landscaping, dominate WPC demand.

- Commercial: The commercial sector is expanding, with WPCs increasingly adopted in offices, hotels, resorts, and public spaces for both functional and decorative purposes.

- Industrial: Industrial usage includes durable storage solutions, pallets, and components where strength and longevity are key considerations.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/76219/

Country-Level Analysis: USA & Germany

United States (USA):

The U.S. is one of the largest markets for wood-plastic composites, driven by robust construction activity and the popularity of outdoor living spaces such as decks and patios. The rise in renovation projects across residential housing has boosted demand. Companies in the U.S. are also making significant investments in expanding manufacturing capacities to cater to rising consumer preference for eco-friendly and low-maintenance materials. The presence of established brands and continuous innovation cements the U.S. position as a leader in WPC adoption.

Germany:

Germany plays a pivotal role in Europe’s WPC market. Stringent environmental regulations and an emphasis on sustainable construction have made WPCs a preferred alternative to traditional timber and plastics. The automotive industry in Germany also supports WPC demand, using these composites in car interiors to meet lightweighting and green standards. Moreover, Germany’s strong infrastructure and innovation in advanced building materials ensure steady market growth, making it one of the most attractive WPC markets in the European region.

Competitor (Commutator) Analysis

The global WPC market is moderately consolidated, with competition shaped by innovation, branding, and expansion strategies. Leading players differentiate themselves through product quality, sustainability credentials, and the ability to scale manufacturing efficiently.

- Strategic Expansions: Companies are heavily investing in expanding production capacity to meet rising demand, particularly in North America and Europe. One major player in the U.S. has recently invested hundreds of millions of dollars in building a large new manufacturing facility to strengthen supply capabilities and meet the surge in home improvement and decking projects.

- Product Innovation: Competitive advantage often stems from introducing new WPC blends with enhanced durability, improved surface finishes, and better weather resistance. Aesthetic versatility—such as natural wood appearances or unique finishes—adds further appeal for consumers and builders.

- Sustainability as a Differentiator: Manufacturers emphasize the recycled content of their WPCs and promote their role in reducing deforestation. Marketing campaigns highlighting circular economy benefits resonate strongly with both regulators and consumers.

- Regional Competition: In Europe, local companies capitalize on regulatory support for sustainable building. In Asia-Pacific, rapid urbanization and infrastructure development are encouraging new entrants to the market. Meanwhile, North American firms benefit from strong branding and large-scale operations.

Press Release Conclusion

The Global Wood-Plastic Composite (WPC) Market is entering a phase of rapid growth and transformation. Valued at USD 8.06 billion in 2024, the industry is projected to achieve a remarkable USD 20.25 billion by 2032, expanding at a 12.2% CAGR. This growth is powered by the convergence of sustainability demands, innovation in materials technology, and robust demand from industries like construction, automotive, and consumer goods.

WPCs are emerging as an essential material for modern, eco-conscious societies. Segmentation reveals their wide-ranging applications—from polyethylene-based decking materials to polypropylene automotive parts—and their ability to meet the needs of residential, commercial, and industrial markets.

Country-level insights highlight the U.S. as a frontrunner, leveraging strong consumer demand and industrial capacity, while Germany showcases Europe’s sustainability-driven momentum in construction and automotive.

On the competitive front, companies are expanding capacity, innovating with new blends and finishes, and positioning WPCs as the go-to material for the future of sustainable living and infrastructure.

As industries and consumers increasingly align toward eco-friendly solutions, wood-plastic composites are well-positioned to bridge the gap between natural appeal and modern durability. The next decade promises not just market expansion but a reshaping of material use across sectors, with WPCs at the forefront of this transformation.