Warehouse Execution System Market Growth Opportunities in E-commerce & Retail Sectors 2030

Global Warehouse Execution System Market Poised to Surpass USD 3.6 Billion by 2030, Driven by Automation and Supply Chain Optimization

Market Definition & Estimation

The Warehouse Execution System (WES) Market has emerged as a vital technological cornerstone in the logistics and supply chain landscape. A WES acts as an intelligent layer between a Warehouse Management System (WMS) and Warehouse Control System (WCS), orchestrating labor, machinery, and inventory in real-time. Unlike traditional systems that function in silos, modern WES platforms integrate advanced algorithms, AI, robotics coordination, and live dashboards, creating a unified and dynamic warehouse environment.

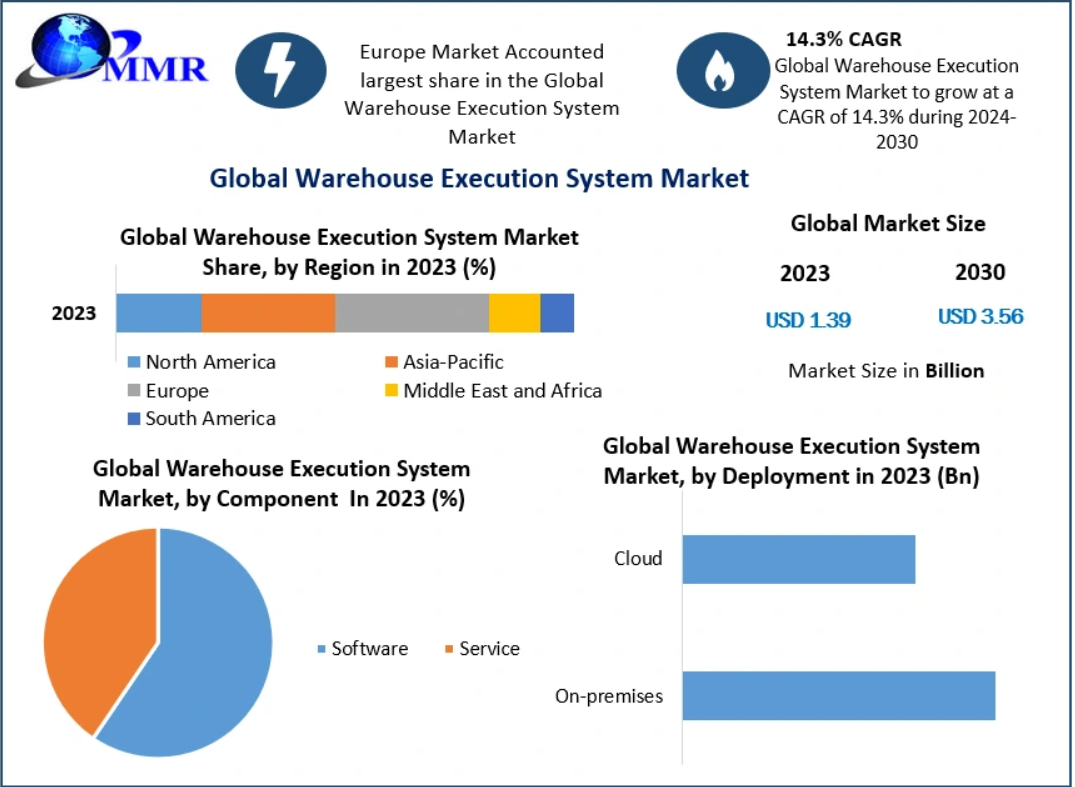

The global WES market was valued at approximately USD 1.39 billion in 2023 and is projected to grow at a robust compound annual growth rate (CAGR) of 14.3%, reaching nearly USD 3.56 billion by 2030. This growth trajectory is being powered by the rapid digitization of supply chains, increased warehouse automation, and the surging demand for real-time order fulfillment.

For in-depth information on this study, visit the following link:https://www.maximizemarketresearch.com/request-sample/114065/

Market Growth Drivers & Opportunities

1. Surge in E-Commerce and Omni-Channel Fulfillment

The exponential rise in global e-commerce has placed significant strain on warehouse operations. With consumers expecting faster deliveries and precise order accuracy, WES platforms have become indispensable. These systems manage order prioritization, eliminate bottlenecks, and enable real-time decision-making, transforming traditional fulfillment centers into agile, high-performance environments.

2. Labor Shortages and Rising Operational Costs

Warehouse labor shortages, combined with increasing wages, have prompted companies to optimize human resource deployment. WES solutions offer labor management tools, resource forecasting, and real-time task allocation. This helps companies achieve greater productivity while minimizing labor-related costs.

3. Integration with Automation and Robotics

The widespread adoption of warehouse automation technologies such as Autonomous Mobile Robots (AMRs), Automated Storage and Retrieval Systems (AS/RS), and conveyors has necessitated a central coordination platform. WES systems are designed to seamlessly integrate with these technologies, orchestrating tasks between human workers and machines to optimize throughput and efficiency.

4. Cloud Deployment and Scalability

Cloud-based WES solutions are rapidly gaining traction due to their scalability, lower upfront investment, and ease of remote management. These platforms allow companies to implement WES solutions without heavy infrastructure costs, making them especially attractive for small and mid-sized enterprises.

5. Predictive Analytics and Real-Time Optimization

Modern WES platforms go beyond basic orchestration to include predictive analytics and intelligent optimization. They enable warehouse managers to forecast order volumes, predict equipment failure, and adapt to real-time changes in inventory levels or labor availability.

Key Opportunities:

- Growth in third-party logistics (3PL) operations is creating high demand for flexible and scalable WES solutions.

- The rise of Industry 4.0 is encouraging manufacturers to invest in intelligent warehouse software.

- Emerging markets are increasingly adopting warehouse automation, offering untapped potential for WES vendors.

Segmentation Analysis

By Component: Software and Services

The market is segmented into software and services. The software segment dominates the market, accounting for the majority share in 2023. This is attributed to the essential role of software in orchestrating warehouse processes, integrating automation equipment, and providing real-time dashboards and analytics. The services segment, which includes consulting, system integration, training, and support, is also expected to grow steadily as companies seek expert guidance in deploying and customizing their systems.

By Deployment Mode: Cloud and On-Premises

Cloud-based deployment holds a larger market share, driven by advantages such as flexibility, scalability, and reduced capital expenditure. This model is especially favored by SMEs looking to modernize their warehouses without significant infrastructure investment. On-premises deployment continues to have strong demand in sectors requiring tight data control and customization, such as pharmaceuticals and aerospace.

By Type: Centralized WES and Embedded WES

Centralized WES systems hold the lion’s share of the market. These platforms manage all warehouse operations from a unified interface, providing end-to-end visibility and control across all systems and equipment. Embedded WES, on the other hand, is typically bundled with specific warehouse automation solutions, offering more focused functionality but less flexibility.

To access more details regarding this research, visit the following webpage:https://www.maximizemarketresearch.com/request-sample/114065/

By End-User Industry

The market serves a variety of industries, including:

- Third-Party Logistics (3PL): This is the largest end-user segment. With growing outsourcing of warehousing functions, 3PL providers are heavily investing in WES to gain operational efficiency and competitive advantage.

- Consumer Electronics: High SKU complexity and rapid order cycles make WES crucial for efficient handling and timely fulfillment.

- Pharmaceuticals: Stringent regulatory compliance and the need for inventory traceability drive demand for real-time WES solutions.

- Food & Beverages: WES enables expiry tracking, temperature monitoring, and accurate inventory rotation.

- Automotive, Healthcare, and General Manufacturing: These sectors benefit from WES through enhanced operational control, traceability, and labor optimization.

By Region

- North America: A mature and dominant market, with the U.S. leading in adoption. High labor costs, advanced logistics networks, and widespread automation support WES growth.

- Europe: A close competitor to North America, led by countries like Germany, France, and the UK. The region’s strong manufacturing base and emphasis on sustainability contribute to robust demand.

- Asia-Pacific: The fastest-growing regional market, propelled by e-commerce expansion, industrial automation, and infrastructure development in countries like China, India, and Japan.

- Latin America and the Middle East & Africa: These regions are expected to witness steady adoption as warehouse modernization and international logistics grow.

Country-Level Analysis

United States

The U.S. leads the global WES market, driven by its large-scale e-commerce industry, tech-savvy retail giants, and high labor costs. Many American warehouses have transitioned to hybrid automation environments, where WES is critical for integrating and synchronizing manual and automated processes. Companies continue to adopt cloud-based solutions for multi-site operations and agile scaling. The demand for real-time inventory visibility, shipping accuracy, and last-mile optimization further accelerates adoption.

Germany

Germany represents the most advanced WES market in Europe. As a global hub for automotive manufacturing and engineering excellence, German warehouses are often highly automated and sophisticated. The country’s strong emphasis on Industry 4.0 and smart factories has led to widespread deployment of centralized WES platforms. Regulatory compliance and a focus on traceability also drive growth in sectors like pharmaceuticals and food processing.

Competitive Landscape (Commutator Analysis)

The WES market is highly competitive and fragmented, with both global giants and regional players vying for market share. The landscape is defined by innovation, strategic partnerships, and industry-specific customization.

Key Players:

- Leading Software Vendors: Major players offer AI-enabled platforms capable of real-time orchestration, demand forecasting, and machine-learning-powered optimization. These systems are often modular and cloud-native, allowing for phased implementation and easy upgrades.

- System Integrators and Automation Specialists: These companies combine WES with physical automation systems like conveyors, sorters, and robotic arms, delivering turnkey solutions tailored to the needs of specific industries.

- Emerging Tech Firms: Innovative startups are entering the market with mobile-first WES solutions, focusing on user-friendly interfaces, IoT integration, and fast deployment times.

Strategic Moves:

- Vendors are investing heavily in R&D to integrate predictive analytics, machine learning, and real-time dashboards into WES platforms.

- Many companies are forming alliances with robotics firms and cloud service providers to offer bundled, future-ready solutions.

- Expansion into Asia-Pacific and Latin America is a key focus, with localized platforms and regional partnerships being developed to tap into emerging demand.

Press Release Conclusion

The global Warehouse Execution System market is experiencing a transformational boom. From an essential logistics tool to a dynamic, AI-powered orchestration platform, WES has evolved to meet the challenges of modern warehousing. Its ability to enhance agility, reduce operational costs, and integrate seamlessly with automation technologies positions it as a cornerstone of the digital supply chain.

As industries around the world adapt to the demands of e-commerce, labor volatility, and just-in-time delivery, the adoption of WES will only accelerate. Cloud computing, machine learning, and IoT integration are reshaping the future of warehouse operations, and companies that invest in robust WES platforms today will lead the competitive race tomorrow.

With a projected market value of USD 3.56 billion by 2030 and double-digit growth across regions and sectors, the WES market stands at the forefront of global supply chain innovation.