Cold Chain Market Challenges: Energy Costs and Sustainability Issues 2030

Cold Chain Market Set to Reach USD 531.87 Billion by 2030, Driven by Rising Demand for Perishable Foods and Pharmaceuticals

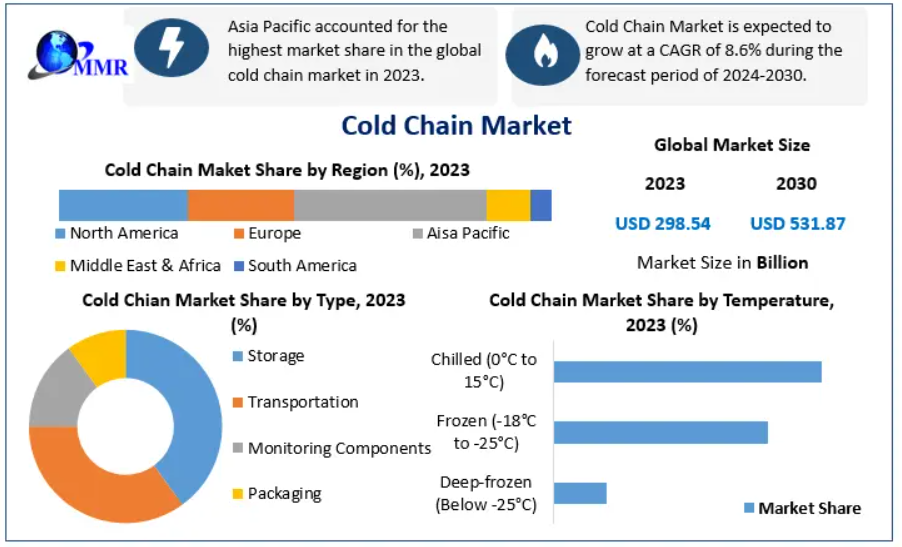

The Cold Chain Market, valued at USD 298.54 billion in 2023, is on a robust growth trajectory, projected to expand at a CAGR of 8.6%, reaching nearly USD 531.87 billion by 2030. This rapid growth is underpinned by shifting consumption patterns toward perishable goods, expanding pharmaceutical logistics needs, and government initiatives to curb food wastage.

Market Overview

A cold chain refers to a temperature-controlled supply chain that relies on refrigerated storage, insulated packaging, and advanced monitoring technologies to safeguard perishable goods during storage and transportation. The system ensures that food, pharmaceuticals, and other sensitive products maintain safety, quality, and extended shelf life.

Today, the cold chain is not just a logistical necessity but also a strategic enabler for global food and healthcare industries. Its integration with advanced IoT, AI-driven monitoring, and eco-friendly packaging is reshaping supply chain resilience worldwide.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/99467/

Key Market Dynamics

Growth Drivers

- Surging demand for perishable food products: Rising health awareness and protein-centric diets are fueling demand for dairy, seafood, and fresh produce.

- Government support to reduce food waste: Policies promoting cold storage infrastructure and subsidies for logistics providers are accelerating adoption.

- Pharmaceutical reliance on cold chain logistics: From vaccines to biopharmaceuticals, temperature-sensitive healthcare products are driving investment in precise cold chain systems.

- Urbanization & frozen food adoption: Consumers are embracing convenient, longer shelf-life frozen meals, boosting demand for storage and distribution networks.

Restraints

- High energy costs and infrastructure investment: Refrigerated warehouses and reefer fleets require substantial upfront capital and operational expenses.

- Fuel price volatility: Increased reliance on refrigerated transport heightens exposure to fuel-related costs.

- Environmental concerns: Energy-intensive operations and refrigerant emissions present sustainability challenges.

Opportunities

- Growth of organized retail: Expansion of supermarkets, hypermarkets, and convenience stores globally is creating steady demand for cold chain storage and transportation.

- Technology integration: IoT-enabled monitoring, AI predictive analytics, and energy-efficient refrigeration systems are set to transform efficiency.

Challenges

- Weak infrastructure in emerging economies: Lack of standardized facilities, fragmented networks, and compliance hurdles limit scalability in developing regions.

Segment Insights

- By Type:

- Storage led the market in 2023 with over 60.3% share, driven by increasing frozen and packaged food consumption.

- Transportation is witnessing strong momentum with rising adoption of reefer trailers, insulated containers, and high-tech refrigerated trucks.

- Monitoring components (hardware & software) are gaining traction as end-users prioritize real-time tracking and temperature regulation.

- By Application:

- Fish, Meat, and Seafood dominated in 2023, accounting for 26.8% of global revenue, supported by technological advances in seafood processing and packaging.

- Processed Food is projected to be the fastest-growing segment, fueled by innovations in packaging materials and rising global trade.

- By Temperature:

- Chilled storage (0°C to 15°C) caters to fresh produce and dairy.

- Frozen (-18°C to -25°C) and Deep Frozen (below -25°C) are critical for meat, seafood, and pharmaceutical applications.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/99467/

Regional Highlights

- Asia Pacific: Dominated the market with 50.64% share in 2023, projected to grow at a CAGR of 13.1%. The region’s rising disposable incomes, expanding healthcare sector, and growing urban population are driving demand for vaccines, frozen meals, and seafood exports.

- North America & Europe: Strong adoption of advanced cold chain technologies but challenged by high energy costs and stricter environmental regulations.

- Middle East, Africa, and South America: Emerging opportunities as food imports and exports expand, though infrastructure gaps remain a bottleneck.

Competitive Landscape

The Cold Chain Market is highly competitive, characterized by global logistics giants and specialized cold storage providers. Leading companies are investing in energy-efficient refrigeration, digital monitoring, and multi-compartment fleets to expand service offerings.

Key players include:

Americold Logistics, Lineage Logistics Holdings, Nichirei Corporation, Burris Logistics, Agro Merchants Group, Kloosterboer, United States Cold Storage, Tippmann Group, VersaCold Logistics Services, Henningsen Cold Storage, NewCold, Sonoco ThermoSafe, UPS, and A.P. Moller – Maersk.

Technological adoption such as RFID tracking, HACCP compliance, and AI-driven predictive monitoring is helping players reduce wastage while ensuring safety and regulatory compliance.

Future Outlook

The cold chain industry is evolving beyond storage and transport into a technology-enabled, sustainability-driven ecosystem. While infrastructure gaps and environmental challenges persist, the surge in organized retail, pharmaceutical logistics, and consumer demand for high-quality perishables is set to keep the market on a strong growth path.

By 2030, with deeper digital integration, energy-efficient practices, and global trade expansion, the cold chain industry will not just be a backbone of food and pharma logistics but a cornerstone of global supply chain resilience.