Automotive Airbag Market Opportunities in Emerging Economies 2032

Global Automotive Airbag Market Poised for Robust Growth — Projected to Soar from USD 15.50 Billion (2024) to USD 33.49 Billion by 2032

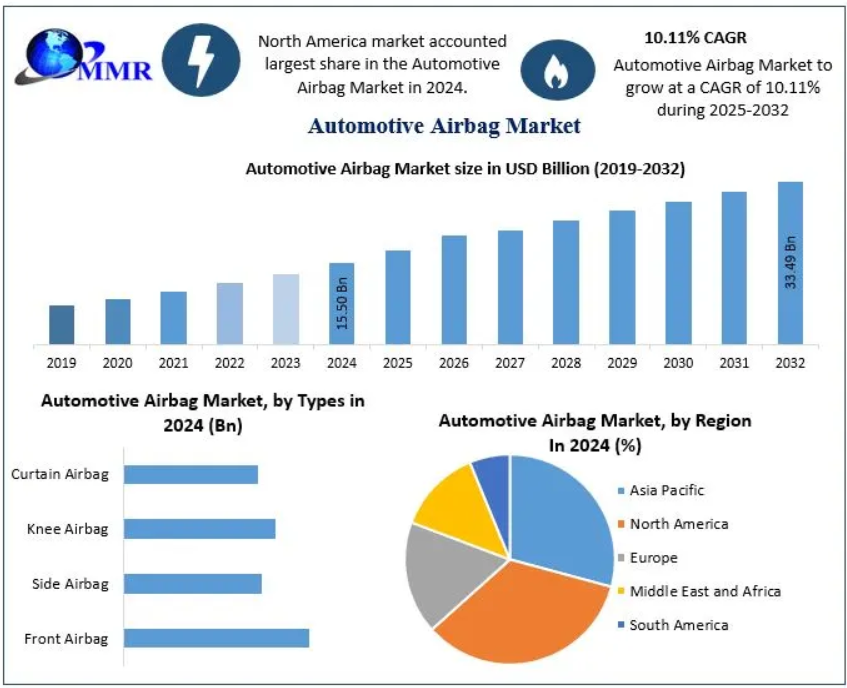

The Global Automotive Airbag Market is witnessing accelerated momentum, fueled by stricter safety regulations, rising consumer demand for advanced protection systems, and continuous technological innovation. The market, valued at USD 15.50 billion in 2024, is projected to nearly double, reaching USD 33.49 billion by 2032, at a compound annual growth rate (CAGR) of 10.11% during the forecast period.

Market Estimation & Definition

Automotive airbags are integral to modern vehicle safety systems, designed to deploy in milliseconds during a collision to reduce injury risks for drivers and passengers. They are typically positioned in multiple areas within a vehicle, including the steering wheel, dashboard, side panels, roofline, and even under the dashboard for knee protection.

The market, valued at USD 15.50 billion in 2024, underscores both widespread regulatory adoption and growing consumer reliance on advanced safety features. Forecasts indicate strong industry growth, with a market size expected to hit USD 33.49 billion by 2032, reflecting not only regulatory pressures but also consumer preference for comprehensive vehicle safety solutions.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/11119/

Market Growth Drivers & Opportunities

Stricter Government Safety Regulations

Global governments have made airbags mandatory in most passenger vehicles, ensuring that even entry-level models are equipped with basic front airbags. These regulations remain the single largest growth driver as automakers comply with safety mandates across key regions.

Consumer Demand for Enhanced Safety

Modern consumers prioritize safety alongside performance and comfort. Increased awareness of road accidents has led to rising expectations for advanced safety systems, including multi-airbag configurations.

Growing Vehicle Production

Expansion in passenger vehicle production, especially SUVs and crossovers, directly fuels demand for airbags. Light commercial vehicles are also increasingly being equipped with advanced safety systems as fleet operators and logistics firms prioritize driver protection.

Technological Advancements

Miniaturized sensors, advanced inflators, and integrated safety modules have improved airbag effectiveness. Developments such as center airbags, external airbags for pedestrians, and smart airbags that adjust deployment force based on crash severity are creating new opportunities.

Rise of Electric & Autonomous Vehicles

As the industry transitions toward electrification and autonomy, specialized airbag systems tailored for new cabin layouts and autonomous driving scenarios are in high demand. These innovations open up lucrative opportunities for manufacturers to cater to next-generation vehicles.

R&D and Collaborations

Leading companies are investing heavily in research, collaborating with automakers to design airbags tailored to new models, lightweight vehicle structures, and alternative propulsion systems. Such partnerships ensure steady innovation and broaden supplier portfolios.

Segmentation Analysis

The global automotive airbag market is segmented by type and vehicle type, with demand patterns showing clear differentiation across categories.

By Type

- Front Airbags: These form the backbone of the market and are mandatory in most regions. Positioned for drivers and front passengers, they remain the largest market segment, offering consistent growth through regulatory enforcement.

- Side Airbags: Positioned in seats or door panels, these protect passengers during side-impact collisions. Rising adoption of side airbags reflects heightened demand for all-round occupant safety, particularly in family vehicles and SUVs.

- Knee Airbags: Installed beneath the dashboard, these are designed to protect passengers’ legs during frontal crashes. While adoption has been slower compared to front and side airbags, demand is increasing in premium and mid-range vehicles.

- Curtain Airbags: Installed along the roofline, curtain airbags protect passengers’ heads in rollover or side-impact crashes. This category is gaining momentum as SUVs and multi-row vehicles dominate consumer preferences worldwide.

By Vehicle Type

- Passenger Cars: Representing the largest share, passenger cars remain the primary growth driver of the airbag market. Safety regulations, coupled with consumer expectations, ensure strong demand across all passenger vehicle categories.

- Light Commercial Vehicles (LCVs): Rising adoption of airbags in delivery vans and fleet vehicles reflects increasing emphasis on protecting drivers in high-utilization vehicles.

- Buses & Trucks: Traditionally slower to adopt airbags, buses and trucks are becoming a new frontier for airbag integration as regulations expand to cover heavy vehicles and commercial passenger transport.

This segmentation underscores a diversified demand landscape, with both regulatory mandates and consumer trends shaping adoption across segments.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/11119/

Country-Level Analysis

United States

The U.S. is one of the fastest-growing automotive airbag markets, with a projected CAGR of 25.7% through 2032—well above the global average. This growth stems from rigorous federal safety mandates, high passenger vehicle production, and strong consumer awareness. The U.S. market is also an innovation hub, with automakers and suppliers collaborating to develop next-generation airbags that integrate seamlessly with advanced driver-assistance systems (ADAS) and autonomous driving technologies.

Germany

Germany, Europe’s automotive hub, is set for steady expansion in the airbag market, with growth projected at a CAGR of 6.2% between 2025 and 2035. The market is estimated to reach USD 2.7 billion by 2035, driven by strict EU safety mandates, widespread adoption in luxury and premium vehicles, and increasing penetration of advanced safety features in electric and hybrid cars. German automakers’ leadership in high-end innovation ensures consistent demand for premium airbag solutions.

Competitor Analysis

The competitive landscape of the automotive airbag market is shaped by a mix of established global players and emerging regional suppliers.

Global Leaders

Major Tier-1 suppliers dominate the market, leveraging economies of scale, advanced R&D facilities, and strong relationships with leading automakers. These companies offer diversified product portfolios, ranging from front and side airbags to specialized knee and curtain systems.

Regional Players

Smaller manufacturers, particularly in Asia-Pacific, are gaining traction by providing cost-effective solutions and localized manufacturing. These firms often serve regional automakers, helping them comply with evolving regulations while maintaining competitive pricing.

Strategic Differentiation

Innovation is the primary battleground. Companies that can design lightweight, adaptive, and sensor-driven airbags are better positioned to secure contracts for new vehicle platforms, especially in the EV and autonomous vehicle categories.

Regulatory Compliance as a Barrier to Entry

Meeting global safety certifications, such as U.S. FMVSS standards and Euro NCAP requirements, requires significant investment in testing and compliance. Established players benefit from these barriers, while new entrants face challenges in achieving large-scale adoption.

Partnerships & Collaborations

Collaborations between automakers and airbag suppliers ensure co-development of products tailored to new vehicle architectures. Such partnerships allow suppliers to remain indispensable in a rapidly evolving automotive landscape.

Press Release Conclusion

The automotive airbag market is on a strong upward trajectory, moving from USD 15.50 billion in 2024 to a projected USD 33.49 billion by 2032, at a CAGR of 10.11%. Growth is powered by global safety mandates, consumer demand for superior protection, rising vehicle production, and technological advancements in sensor-driven, modular, and adaptive airbag systems.

Market segmentation reveals diversified adoption across front, side, knee, and curtain airbags, as well as across passenger cars, light commercial vehicles, and heavy-duty vehicles. While front airbags remain foundational, side and curtain airbags are gaining traction as holistic safety solutions become the consumer standard.

Regionally, the United States is expected to lead with a remarkable CAGR of 25.7%, while Germany is projected to steadily expand at 6.2% CAGR, reaching USD 2.7 billion by 2035. Together, these markets illustrate both high-growth opportunities and stable, innovation-driven expansion.

Competition in the market is defined by technological innovation, regulatory compliance, and strong OEM partnerships. Established Tier-1 suppliers continue to dominate, but regional players are making inroads by focusing on cost efficiency and localized solutions.

For stakeholders across the automotive value chain—including automakers, suppliers, and investors—the global automotive airbag market offers a lucrative opportunity, driven by the convergence of safety imperatives and technological evolution. Companies that prioritize R&D, build strong OEM partnerships, and align with regulatory frameworks are positioned to emerge as long-term leaders in this expanding market.